Semiconductors are the backbone of modern life, powering everything from smartphones to AI systems and defense technologies. But here's the catch: the global supply chain for these chips is highly concentrated, creating vulnerabilities and reshaping global power dynamics.

Key Takeaways:

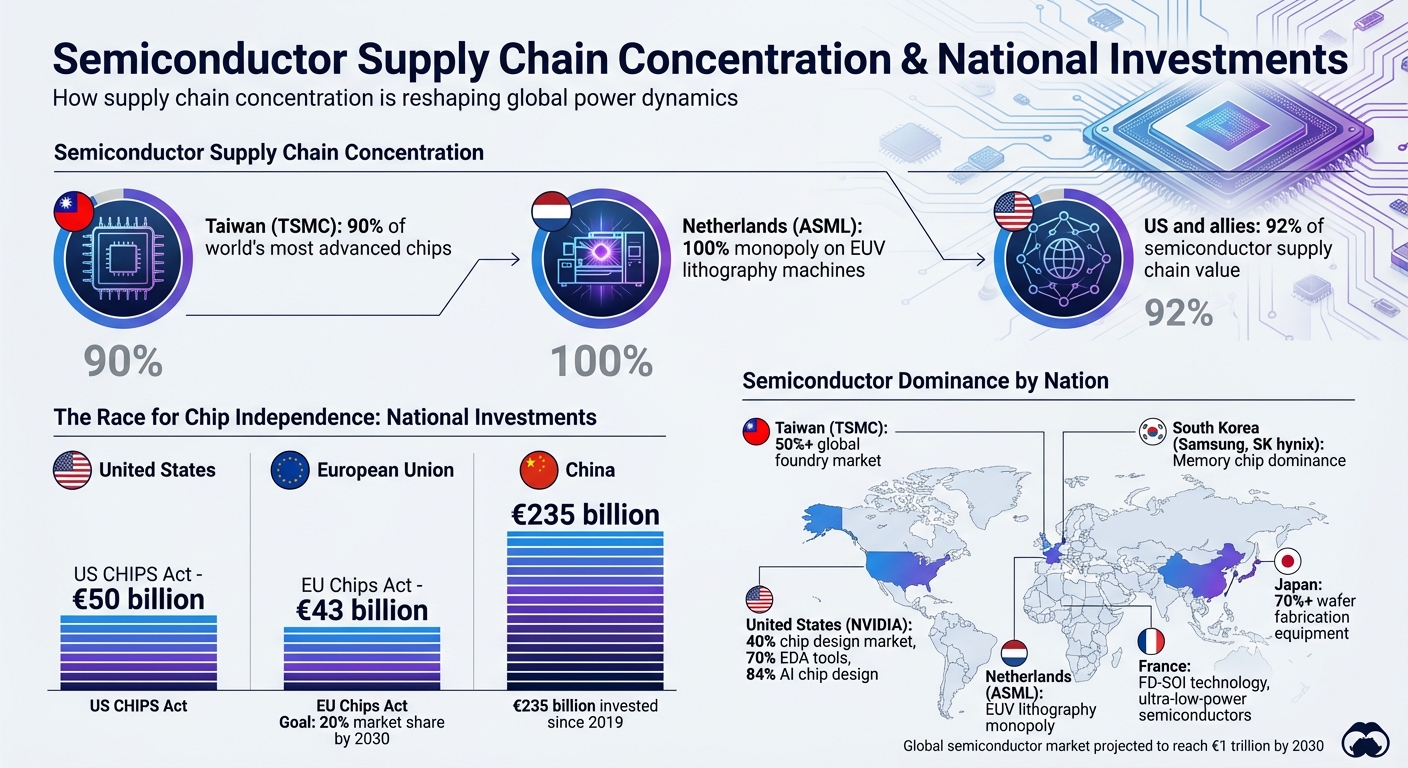

- Taiwan's TSMC produces 90% of the world's most advanced chips, while Netherlands' ASML holds a monopoly on EUV lithography machines.

- The US and allies control 92% of the semiconductor supply chain value, leaving industries globally exposed to disruptions.

- Nations are racing to secure chip independence:

- US CHIPS Act: €50 billion to revive domestic production.

- EU Chips Act: €43 billion to boost Europe's share to 20% by 2030.

- China: €235 billion invested since 2019 to counter restrictions and grow local capacity.

France's Role:

France focuses on mature-node semiconductors and ultra-low-power technologies, steering clear of direct competition in advanced nodes. Key players like STMicroelectronics, Soitec, and CEA-Leti are driving this effort, supported by the France 2030 plan and the European Chips Act.

The stakes are high: control over semiconductors means control over AI, defense, and economic resilience. This global race is not just about technology - it's about power.

Global Semiconductor Supply Chain: Market Share and National Investments by Region

Chips, Power, and Politics: The Geopolitics of Semiconductor Supply Chains

sbb-itb-e314c3b

Major Players in the Semiconductor Industry

A handful of nations and companies dominate the semiconductor landscape, controlling various aspects of chip production and equipment manufacturing. Taiwan, South Korea, and the United States are key players in chip production, while Europe plays a vital role in manufacturing equipment and specialized technologies. This concentration of expertise presents both opportunities and challenges for the global economy.

Nations Leading Chip Production

Taiwan is the epicenter of global chip manufacturing, thanks to TSMC (Taiwan Semiconductor Manufacturing Company), which accounts for over 50% of the global foundry market [10]. In March 2025, TSMC announced a $165 billion investment to expand its operations in Phoenix, Arizona. The project, led by Chairman and CEO Dr. C.C. Wei, includes three new fabrication plants and two advanced packaging facilities, promising to create a significant number of high-tech jobs [7].

South Korea dominates the memory chip market through Samsung and SK hynix, holding a strong grip on DRAM and NAND technologies. SK hynix has become especially important for AI systems with its High Bandwidth Memory (HBM) technology. Between August 2024 and January 2026, the company committed $3.87 billion to build a next-generation packaging facility at Purdue University Research Park in Indiana. Mass production of advanced HBM chips for AI GPUs is set to begin in late 2028 [9].

The United States leads in chip design and software, controlling over 40% of the global chip design market and around 70% of Electronic Design Automation (EDA) tools, with companies like Cadence, Synopsys, and Mentor at the forefront [8]. NVIDIA alone commands 84% of the global AI chip design market [1]. In September 2024, Intel secured up to $3 billion in grants from the U.S. Department of Defense and Department of Commerce to support its "Secure Enclave" program, which focuses on producing microelectronics for national security applications [9].

Other nations also play pivotal roles in the global semiconductor supply chain. Japan is a leader in semiconductor materials, chemicals, and assembly equipment. Companies like Shin‑Etsu, Tokyo Electron, and Advantest supply over 70% of the world's wafer fabrication equipment, alongside U.S. firms [8]. Meanwhile, China is making strides in mature-node manufacturing and assembly, investing over €235 billion in its semiconductor sector since 2019 to counter U.S. export restrictions [3].

Europe's Return to the Semiconductor Race

Europe is reasserting itself in the semiconductor industry by leveraging its existing strengths. Rather than competing directly in advanced logic chips, Europe focuses on areas like manufacturing equipment, power semiconductors, and mature-node technologies, which are critical for automotive and industrial applications. This approach allows Europe to complement, rather than compete with, the capabilities of other major players.

The Netherlands plays a crucial role through ASML, which holds a monopoly on Extreme Ultraviolet (EUV) lithography machines. These machines are indispensable for producing the most advanced chips [10]. Meanwhile, France contributes through companies like STMicroelectronics and Soitec, which specialize in FD‑SOI (Fully Depleted Silicon‑On‑Insulator) technology for ultra-low-power applications. In a significant move, STMicroelectronics and GlobalFoundries are investing €7.5 billion in Crolles, France, to produce 300-mm FD‑SOI wafers [12]. On 30 January 2026, France inaugurated the FAMES pilot line, dedicated to advancing ultra-low-power semiconductors, further solidifying its role in the European semiconductor ecosystem [12].

By late 2025, the European Commission approved state aid for semiconductor projects, representing over €31.5 billion in combined public and private investment [12]. Daniel Gros of the European Commission JRC encapsulated the global dynamic:

"The software comes from the US, the fabs are in Asia and Europe has a strong position in the machines to produce the most advanced (logic) chips" [6].

Europe's strategy aims to bolster its existing strengths while enhancing autonomy across the semiconductor supply chain.

France's Position in the Global Semiconductor Ecosystem

France has carved out a niche in the semiconductor industry by focusing on specialised technologies rather than large-scale production. Its expertise lies in ultra-low-power semiconductors, advanced substrates, and precision metrology tools, all of which play a critical role in the global supply chain. This targeted approach allows France to stand out in specific areas of chip technology.

France's Semiconductor Capabilities and Developments

The Grenoble region is the heart of France's semiconductor activity, with the renowned CEA-Leti research institute at its core. This area has fostered over 75 startups and has become a cornerstone of France's microelectronics sector [13]. Sébastien Dauvé, Director at CEA-Leti, highlighted the importance of self-reliance:

"We needed to regain some autonomy and sovereignty over our capacity to manufacture things on our own territory." [13]

One of France's standout advancements is its FD-SOI (Fully Depleted Silicon-On-Insulator) technology, known for its ultra-low power consumption - ideal for 5G, automotive systems, and IoT devices. A major milestone came in 2023 with the launch of the Crolles mega-factory, a collaboration between STMicroelectronics and GlobalFoundries. This facility produces 300-mm FD-SOI wafers for automotive, IoT, and mobile applications. Backed by €2.9 billion in French government funding as part of a €7.5 billion project, it represents a significant investment in the sector [13][14].

Soitec, another key player, leads the way in semiconductor substrates, holding over 4,000 patents and dedicating 11% of its revenue to research and development [13]. In late 2023, the company announced a €1 billion investment plan, with nearly half allocated to expanding its Bernin facilities for SmartSiC™ technology. These silicon carbide substrates enhance energy efficiency in electric vehicles and data centres. Pierre Barnabé, Soitec's CEO, underscored the challenges of global competition:

"Support for the industry is essential if France is to remain competitive in a global market facing strong pressure from the United States and Asian countries." [13]

In addition to manufacturing, France plays a key role in semiconductor infrastructure. UnitySC, based in Grenoble, specialises in metrology and inspection tools. In 2022, the company secured €48 million to scale up production of equipment designed to detect microscopic defects during the 600+ steps of chip fabrication [13]. Graham Lynch, UnitySC's CMO, spoke to France's strategic foresight:

"France has always been 'ahead of the curve' by treating the electronics supply chain as a deeply strategic part of its economy." [13]

On 30 January 2026, France launched the FAMES pilot line, a project aimed at transitioning ultra-low-power semiconductors from research to industrial production [14][12]. These innovations are supported by initiatives like France 2030 and the European Chips Act, ensuring sustained development in this critical sector.

France 2030 and the European Chips Act

France's semiconductor ambitions align with the European Chips Act, a plan to double the EU's global market share to 20% by 2030 [13][14]. The France 2030 plan dedicates €5 billion to strengthening the national electronics sector, focusing on opportunities in automotive, industrial, and IoT applications [13].

The European Chips Act marks a shift in EU industrial policy, enabling France to provide subsidies for advanced semiconductor facilities [11][15]. Under Pillar I (the Chips for Europe Initiative), France hosts cutting-edge pilot lines, while Pillar II supports large-scale manufacturing efforts like the Crolles mega-factory.

In February 2026, the EU invested €700 million in NanoIC, the largest pilot line under the Chips Act so far [14][12]. The European Commission emphasised the importance of this initiative:

"The European Chips Act will reinforce the semiconductor ecosystem in the EU, ensure the resilience of supply chains and reduce external dependencies." [14]

France's strategy centres on its strengths in FD-SOI and power semiconductors, avoiding direct competition in advanced logic chips dominated by Taiwan and South Korea. This approach allows France to reinforce its existing capabilities while addressing supply chain vulnerabilities highlighted by recent global disruptions. In doing so, it contributes to Europe's broader goal of reducing geopolitical dependencies in semiconductor manufacturing.

| Key French Player | Primary Specialisation | Key Technology/Project |

|---|---|---|

| STMicroelectronics | Integrated Device Manufacturing | 300-mm FD-SOI (Crolles Mega-factory) |

| Soitec | Semiconductor Materials/Substrates | Smart Cut™, SmartSiC™ |

| UnitySC | Metrology & Inspection | TSV monitoring and defect detection |

| CEA-Leti | Research & Development | FAMES and NanoIC pilot lines |

| GlobalFoundries | Foundry Services | Joint venture in Crolles facility |

These efforts highlight France's commitment to strengthening its semiconductor niche and maintaining a competitive edge in the global market.

AI and Geopolitics: How Technology Drives Semiconductor Demand

AI's Impact on Chip Design and Manufacturing

The rise of artificial intelligence is reshaping not just technology but also global power structures, particularly in the semiconductor industry. Training a state-of-the-art AI algorithm today takes about one month and costs approximately €95 million [16]. This immense computational demand has made specialized AI chips - like GPUs, FPGAs, and ASICs - indispensable.

These chips stand out because they excel at parallel processing and are optimized for the arithmetic operations required by AI tasks [16]. With Moore's Law slowing, the focus has shifted toward creating custom circuits that continue to push performance boundaries.

The production of these chips is a significant geopolitical factor. Taiwan's TSMC produces over 90% of the world’s most advanced semiconductors [17], giving certain regions and companies enormous influence over access to cutting-edge AI technology. Saif M. Khan from CSET highlights this dependency:

"The success of modern AI techniques relies on computation on a scale unimaginable even a few years ago." [16]

Beyond commercial applications, high-performance AI chips power advancements in defense, cryptography, and surveillance systems [4]. Export controls on vital equipment, such as ASML's EUV machines, have further escalated global competition. The US, the Netherlands, and Japan have imposed restrictions to curb China's progress in AI while maintaining their technological advantage [1][18].

This competitive environment is driving nations to invest in building their own robust, independent AI and semiconductor capabilities.

France's Focus on Emerging Technologies

Amid the growing demand for specialized AI chips, France is making strategic moves to strengthen its AI infrastructure. The country is positioning itself as a key player in the global AI race, focusing on reducing dependency on foreign technology [19]. One of France’s standout advantages is its access to low-carbon nuclear energy, an attractive feature for energy-intensive AI data centers. By 2030, global data-center electricity consumption is expected to more than double, reaching 945 TWh - about 3% of worldwide energy use [19].

Through its France 2030 investment plan, the country has successfully drawn €109 billion in private capital to develop sovereign AI capabilities [19]. A notable example is the 1.4 GW data-center campus that opened near Paris in mid-2025. Backed by a consortium including MGX (UAE), Brookfield (Canada), Bpifrance, and Iliad, this facility is equipped with 18,000 Nvidia Grace Blackwell GPUs, providing significant AI-ready capacity for the region [19].

France is also playing a central role in the European Semicon Coalition, collaborating with nine EU member states to bolster the local semiconductor industry and secure supply chains [17]. Currently, France’s compute intensity is around 75 PFLOPs per €1 trillion of GDP, with public supercomputing performance reaching 0.42 exaflops as of mid-2025 [19].

These initiatives highlight France’s determination to establish itself as a leader in AI and semiconductor technologies, ensuring greater autonomy in a rapidly evolving global landscape.

How Supply Chain Disruptions Affect Geopolitics and Innovation

US-China Rivalry and the Drive for Chip Independence

The 2021 semiconductor shortage hit hard, stripping an estimated €225 billion from the US GDP and cutting global car production by 7.7 million vehicles [8]. The crisis highlighted vulnerabilities in the supply chain, especially for mature-node semiconductors that power everyday devices.

This fragility has intensified the already heated rivalry between the US and China. American export controls now target key bottlenecks, blocking China's access to advanced chips like Nvidia's A100 and H100, as well as critical manufacturing tools such as ASML's EUV lithography machines [21]. The goal? To slow China's advancements in AI and military tech while keeping Western technological dominance intact.

China, however, hasn’t stood idle. Since 2019, it has poured over €235 billion into semiconductor manufacturing, tripling its domestic capacity to around 3 million wafers per month [3]. In a surprising move, Huawei unveiled its Mate 60 Pro smartphone in September 2023, powered by the 7nm Kirin 9000s processor. Manufactured by China's SMIC using Deep Ultraviolet (DUV) lithography, this achievement demonstrated that China's tech capabilities are advancing faster than many Western policymakers expected [21].

Bruce Andrews, Corporate Vice President at Intel, summed up the stakes perfectly:

"The way that the oil reserves defined the economics and geopolitics of the last 50 years, semiconductors are going to do that for the next 50." [2]

China is also doubling down on talent. Through its "Qiming" programme, it offers signing bonuses ranging from €395,000 to €660,000 to attract top-tier semiconductor experts [21]. Jiangsu Province has committed €70 million annually to support local chip firms, while the "Big Fund" launched a new €38.5 billion initiative in 2023, following a €25.4 billion fund established in 2019 [21].

This technological decoupling has global implications. Nations increasingly see AI as a strategic resource, comparable to military strength, and are developing "Sovereign AI" systems tailored to their own values and regulations [3]. These shifts are driving ambitious national efforts to diversify supply chains.

Strategies for Supply Chain Diversification

Countries are responding to supply chain vulnerabilities with massive financial investments. For instance:

- The US CHIPS and Science Act has allocated €50 billion in subsidies.

- The European Union's Chips Act offers over €43 billion in funding [2].

- Japan is committing €12.2 billion, and India has launched a Semiconductor Mission worth approximately €9.4 billion [2].

These measures mark a shift from prioritizing efficiency to emphasizing resilience. As Gina Raimondo, US Secretary of Commerce, explained:

"Previously, the United States produced nearly 40% of the world's chips. Now, we produce just 12%. We're changing that with the CHIPS and Science Act." [2]

Beyond financial incentives, nations are forging partnerships to diversify supply chains with "friendly" countries. In June 2022, the US Department of State allocated €470 million from the CHIPS Act to expand semiconductor production in seven partner nations, including Vietnam, the Philippines, and Costa Rica [2]. Micron Technology, for example, announced a new €2.8 billion chip facility in India in October 2023, supported by government subsidies [2].

The shift in assembly, testing, and packaging is also notable, moving from China and Taiwan to regions like Southeast Asia, Latin America, and Eastern Europe [20]. South Korea and Taiwan are adopting a dual approach: high-end capacity at home and lower-end production abroad [5].

Global investment in wafer fabrication is expected to soar to €2.2 trillion between 2024 and 2032, a significant leap from the €677 billion invested in the previous decade [20]. The US share of advanced chip fabrication (nodes newer than 10nm) is forecasted to rise from 0% in 2022 to 28% by 2032 [20].

Still, geopolitical tensions complicate these plans. In August 2023, Intel had to abandon its €5.1 billion acquisition of Tower Semiconductor after Chinese regulators withheld approval, showcasing China's ability to exert regulatory pressure on foreign expansions [21].

While many nations focus on advanced nodes, France has carved out a niche in mature-node semiconductors to ensure stability in critical industries.

France's Mature-Node Expertise as a Competitive Edge

France has strategically positioned itself in the mature-node semiconductor market, an area crucial for industries like automotive, healthcare, and manufacturing. Through Soitec, one of the top five global silicon wafer manufacturers, France plays a pivotal role, contributing to the 95% global market share controlled by these companies as of 2020 [8].

Mature-node semiconductors (28nm and above) are often overlooked but remain indispensable. As a report from CSIS highlighted:

"Legacy chips are at least as critical as advanced chips both in terms of economic importance and national security." [21]

France's expertise in materials gives it a key advantage. The European Chips Act, which mobilizes over €43 billion in combined public and private investments, aims to double the EU's global semiconductor market share to 20% by 2030 [22]. Margrethe Vestager, Executive Vice President of the European Commission, clarified this approach:

"This is not an act of protectionism; this is not trying to be self-sufficient. This is to have a much stronger weight in the global ecosystem of semiconductors." [2]

Conclusion: The Future of Geopolitics and Semiconductors

Semiconductors have shifted from being purely economic assets to becoming key players in national security and global political influence. As the global semiconductor market is expected to hit €1 trillion by 2030 [23], control over chip supply chains will directly impact leadership in AI, defense, and technological progress.

France has carved out a strategic role in this shifting landscape. With the EU Chips Act providing €43 billion in funding and its participation in the nine-member Semicon Coalition, France is aligning its efforts with European partners to secure long-term opportunities in the semiconductor sector [1]. By focusing on mature-node technologies and specialized materials, with companies like Soitec leading the way, France has developed a strong position in areas where older-generation chips remain essential for economic and security purposes. This focus lays the groundwork for innovative supply chain strategies.

The future will depend heavily on "right-shoring" strategies and strong partnerships. As Alexandre Ferreira Gomes and Jelle van den Wijngaard from Clingendael observed:

"A stronger domestic ecosystem will help Europe handle disruption, create jobs, and reduce dependency on global chokepoints" [1].

Realizing this vision demands not just financial resources but also platforms that encourage collaboration across the AI and semiconductor industries.

One such platform is the RAISE Summit, held at the Carrousel du Louvre in Paris. With over 9,000 attendees, this event facilitates critical cross-industry discussions to address geopolitical challenges while advancing technological innovation. In a world where control over key semiconductor processes - like EUV lithography, advanced chip design, and precision fabrication - defines AI capabilities [1], cooperation between nations, companies, and research institutions has never been more crucial.

As these strategies take shape, the next decade will likely see semiconductor supply chains redefining global power dynamics, much like oil reserves once did. The ability to produce chips and advance AI technologies now directly influences national strength. With its targeted focus on mature-node technologies and strong European collaboration, France is well-positioned to play a central role in this evolving geopolitical and technological landscape.

FAQs

Why is EUV lithography such a major chokepoint?

EUV lithography represents a significant bottleneck in semiconductor manufacturing due to ASML's monopoly on these machines. These tools are indispensable for creating advanced semiconductors. The technology's development involved decades of research and intense collaboration, making it nearly impossible for other regions to duplicate or sidestep this essential process.

What would a disruption in Taiwan mean for AI and defence?

Taiwan's role in global semiconductor production is massive, with the country manufacturing over 90% of the world's advanced chips. These semiconductors are the backbone of AI systems and military technologies, making them indispensable. A disruption in Taiwan's production could send shockwaves through global supply chains, stalling technological advancements and impacting strategic military capabilities. This underscores just how critical semiconductor manufacturing is when it comes to shaping global power and stability.

How does France’s FD‑SOI focus improve Europe’s chip resilience?

France’s focus on FD-SOI technology plays a key role in boosting Europe’s semiconductor independence. By supporting the development of secure, energy-efficient, and affordable chips, this approach helps reduce dependence on external supply chains. At the same time, it enhances local manufacturing capabilities, paving the way for greater self-reliance in European technology.